Establishing a firm groundwork in your financial life can feel like constructing a monument in shifting sands. Yet, when you prioritize core necessities and embrace proven strategies, you can stand resilient in the face of economic storms. This article offers an inspiring, hands-on guide to fortifying your economic future and achieving lasting security.

By understanding the essential elements of economic stability—and applying practical methods—you can move confidently toward your goals. Let’s explore how to build your foundation brick by brick.

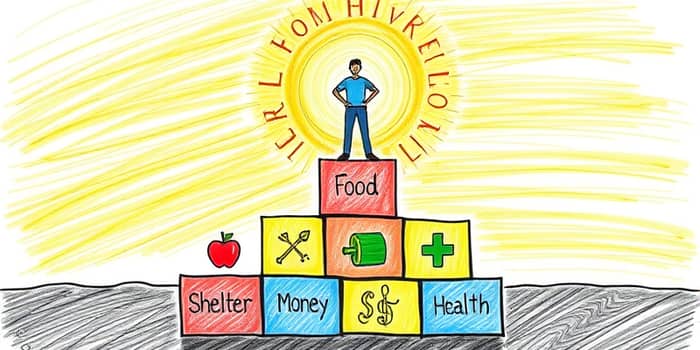

Understanding Your Four Walls

At the very base of your economic structure lie the non-negotiable basics, known as the Four Walls. These are the essentials you must cover before addressing anything else.

- Food

- Shelter

- Utilities

- Transportation

Ensuring you can cover basic living costs each month establishes security. Without reliable access to nourishment, a roof, power, and mobility, every other financial plan loses its stability.

The Four Pillars of Personal Finance

Once your walls stand strong, you need structural supports to hold them aloft. The Four Pillars give shape and resilience to your economic foundation.

- Income — Money earned from employment, investments, or side ventures

- Expenses — Fixed and variable costs that dictate your cash flow

- Assets — Resources and holdings that build wealth over time

- Debts — Obligations that must be managed and repaid

By examining how these pillars support your Four Walls, you gain insight into where to reinforce or adjust your efforts. Strong pillars allow you to weather monthly bills, unexpected medical costs, and life changes.

Key Building Blocks for Stability

Beyond the walls and pillars, specific strategies serve as the individual blocks you stack to reach lasting security. Each block combines to create a comprehensive plan.

Mastering your monthly budget is the first critical step. When you track every dollar in and out, you gain clarity on spending habits.

Create categories for fixed costs (rent, insurance) versus variable costs (dining, entertainment). Use the wealth equation—[WHAT YOU EARN] minus [WHAT YOU SPEND]—to ensure you maintain positive cash flow each cycle.

The next block is building an emergency reserve. A starter fund of $500–$1,000 shields you from small shocks. Ultimately, aim for three to six months’ worth of expenses.

Keep these funds in accessible accounts so you can access emergency funds instantly when life takes an unexpected turn.

Managing and reducing debt is equally transformative. Focus on high-interest balances first, such as credit card debt, since these can compound quickly and erode your progress. Adopting the avalanche or snowball method ensures you paying down high-interest debt efficiently.

On the income side, treat every dollar coming in as an opportunity. If your earnings fluctuate, build your budget around your lowest monthly income to avoid shortfalls. Remember to pay yourself first by automatically diverting a portion of each paycheck into savings or investment accounts.

Peek closely at your discretionary spending. Subtle costs—daily coffee runs, monthly subscriptions—can drain your wallet over time. By separating needs from wants, you free up resources to accelerate debt repayment and boost savings, creating sustainable long-term financial growth.

Finally, protect your assets through comprehensive risk management. Insurance policies—health, renters or homeowners, auto—act as shields against catastrophic expenses. Review coverage periodically to confirm you’re neither underinsured nor overpaying.

Long-term planning ties every block together. Map out retirement contributions, investment goals, and an estate plan. Regularly revisit your strategy, adapting to life events like career changes, growing families, or market shifts. Logical adjustments ensure you remain on course rather than reacting emotionally to volatility.

Economic Stability in Broader Contexts

Financial foundations extend beyond personal budgets. In architecture and development, stability means designing cost-effective, sustainable buildings that endure market cycles. Planners incorporate green materials and flexible layouts to safeguard against supply chain issues and shifting demands.

On a societal level, economic stability touches public health. Food security, stable housing, and employment opportunities determine how communities navigate crises—from natural disasters to pandemics. A population with robust emergency savings is better equipped to evacuate, recover, and rebuild.

At the macro level, governments pursue policies that foster fair trade, reduce corruption, and support inclusive growth. When power structures and financial systems remain transparent, citizens enjoy greater confidence in their institutions, reinforcing stability across the board.

Milestones and Benchmarks

Tracking your progress with clear milestones helps maintain momentum. Three reliable benchmarks include:

• Maintaining three to six months of living expenses in emergency savings.

• Staying consistently on track with retirement planning contributions.

• Paying down burdensome, high-interest debt.

When you reach these markers, you’ll feel a profound sense of accomplishment and renewed motivation to tackle the next phase of growth.

Essential Skills for Financial Mastery

- Earning — Maximizing income sources and negotiating better terms

- Spending — Making logical decisions over emotions and trends

- Saving — Consistent surplus income contributions into secure accounts

Developing these skills transforms abstract principles into everyday habits. Over time, each deliberate choice compounds, turning small gains into significant achievements.

Supporting Principles

Anchoring your journey are a few timeless tenets: always create a plan and commit to it, prioritize logical decisions over impulsive buys, and protect your savings against unnecessary risk. By consistently channeling surplus income toward your goals and maintaining disciplined spending, you cultivate both freedom and resilience.

Building a robust economic foundation isn’t a one-time effort; it’s a lifelong pursuit. Celebrate each victory—no matter how small—and treat setbacks as learning opportunities. With patience, perseverance, and the right approach, you can achieve lasting economic stability and peace of mind.

Now is the moment to lay your first block. Start today, and watch as your financial structure grows stronger with every deliberate action.

References

- https://www.studysmarter.co.uk/explanations/architecture/real-estate/economic-stability/

- https://navicoresolutions.org/resources/blog/the-foundations-of-personal-finance-building-stability-and-resilience

- https://www.edwardjones.com/us-en/market-news-insights/guidance-perspective/how-be-financially-stable

- https://www.newfront.com/blog/5-building-blocks-of-financial-resilience-during-turbulent-times

- https://lifestyle.sustainability-directory.com/area/economic-stability-building/resource/2/

- https://myhome.freddiemac.com/blog/financial-education/building-blocks-wealth-constructing-stable-financial-future-your-family

- https://lifestyle.sustainability-directory.com/area/economic-stability-foundations/resource/6/

- https://www.heritagefederal.org/home/talking-cents/blogs/the-building-blocks-of-personal-finance

- https://www.cdc.gov/prepyourhealth/discussionguides/economicstability.htm

- https://www.getrichslowly.org/earning-spending-and-saving-the-building-blocks-of-personal-finance/

- https://www.aspeninstitute.org/publications/short-term-financial-stability-a-foundation-for-security-and-well-being/

- https://www.wealthmorning.com/2024/09/11/652763/the-financial-building-blocks-for-a-successful-professional-life/

- https://personal-finance.extension.org/investing-unit-1-building-blocks/

- https://upward-mobility.urban.org/framework